Aftermarket decline continues in first half of 2025 with pricing playing its part

The automotive aftermarket has continued its challenging start to 2025 – with trading numbers down on last year’s figures – according to Factor Sales.

After noting a 3.1% decline in sales volume and a 3% drop in revenue during the first nine weeks, the leading market measurement provider can now confirm that this downward trend has persisted. Over the first 22 weeks of 2025, sales are down 4.83% and revenue has declined by 5.82% compared to the same period in 2024.

However, when compared to the same period in 2023, the picture is more stable: unit sales are down by just 2.16%, and revenue is broadly flat with a marginal 0.03% increase.

Price increases offset volume decline

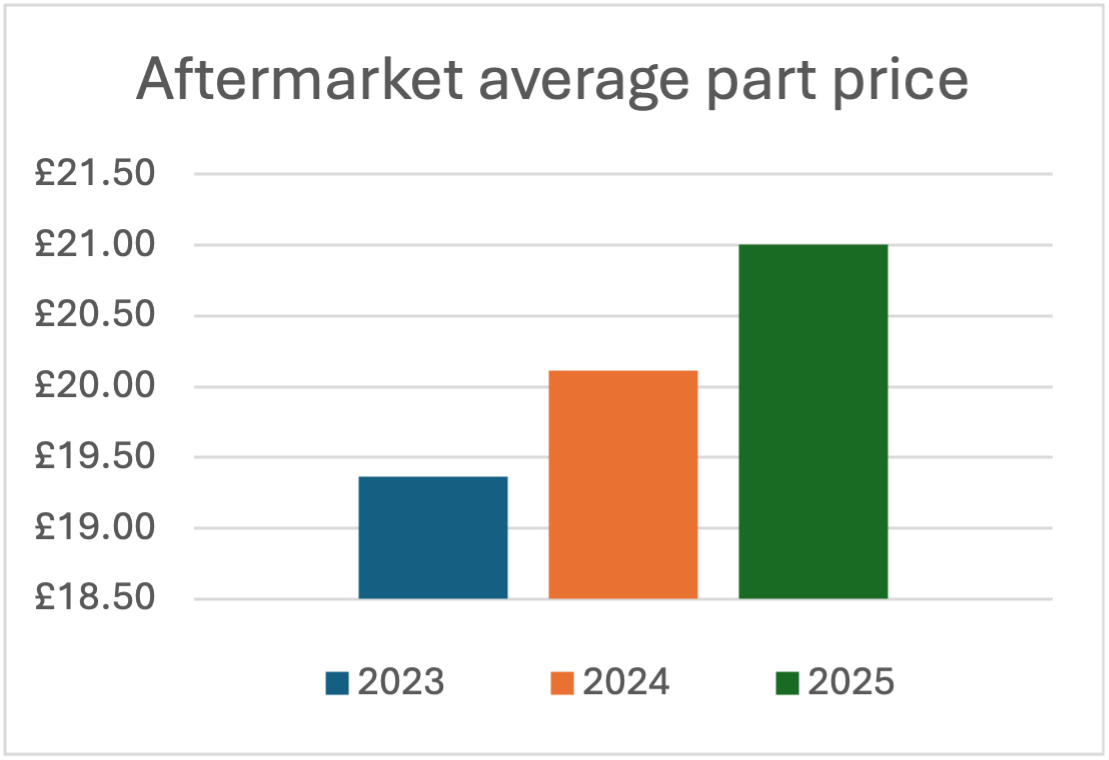

The divergence between revenue and volume reflects a rise in average part prices. The average unit value has increased to £21.01, up from £20.12 in 2024 and £19.36 in 2023.

Primarily, this is driven by increased sales in higher-value categories – such as body and exhaust components – alongside a drop in sales of lower-value miscellaneous items. These changes are helping to offset broader pricing pressures seen across the market, including increased promotional activity and competitive pricing from national distributors.

Category performance insights

Despite the overall market challenges, several component categories have shown positive signs. The cooling and heating segment, for example, continues to perform strongly. Engine and service part categories have recovered from early-year lows, now standing at just 1.5% and 1.3% down in revenue, respectively. Notably, the engine components category has seen a 2% increase in unit sales.

Conversely, braking continues to underperform, with a 9.5% decline in revenue and an 11% fall in unit sales.

“We will continue to monitor the trends”

Factor Sales Business Development Manager, Alex Jenner, said: “This latest data is concerning and while it is difficult to pinpoint exactly why, looking back to 2023 when the market was broadly flat in terms of value, the recent price increases would indicate that they are now playing a significant role.

“Despite the broader decline, some areas are showing resilience, and I hope that other component categories will do the same as we move into the second part of 2025. We will continue to monitor the trends and provide our latest report in Q3.”